Unlocking Investment Trusts

This blog post and presentation was not prepared by professional investors, it’s not a recommendation to buy or sell any securities and every investor should undertake their own independent research prior to investing. The information was prepared a few months ago and might be out of date.

Full credit goes to Andrew Driver from our local FI Group.

Introduction

01 – Reference Material

02 – What Investment Trusts are, and more importantly what they are not.

03 – How Investment Trusts work

04 – Pros and Cons for Investment Trusts

05 – Some Examples of Investment Trusts

06 – Dividend Heroes & Non Dividend Paying Options

07 – Irish Investors and Taxation on Funds

08 – ETF v Investment Trusts (IT) Fees Model (Comparison table)

Or click here

01 Reference Material

01 – Investment Trusts – Unlocking The City’s Best Kept Secret (2nd Edition) By John Baron

02 – The Investment Trusts Handbook 2020 By Jonathan Davis.

03 – Association of Investment Companies. (AIC) www.theaic.co.uk

04 – Money Makers Podcast

05 – IT Investor (Blog) Exploring the world of investment trusts www.itinvestor.co.uk

02 – What Investment Trusts are, and

more importantly what they are not.

A – What are Investment Trusts

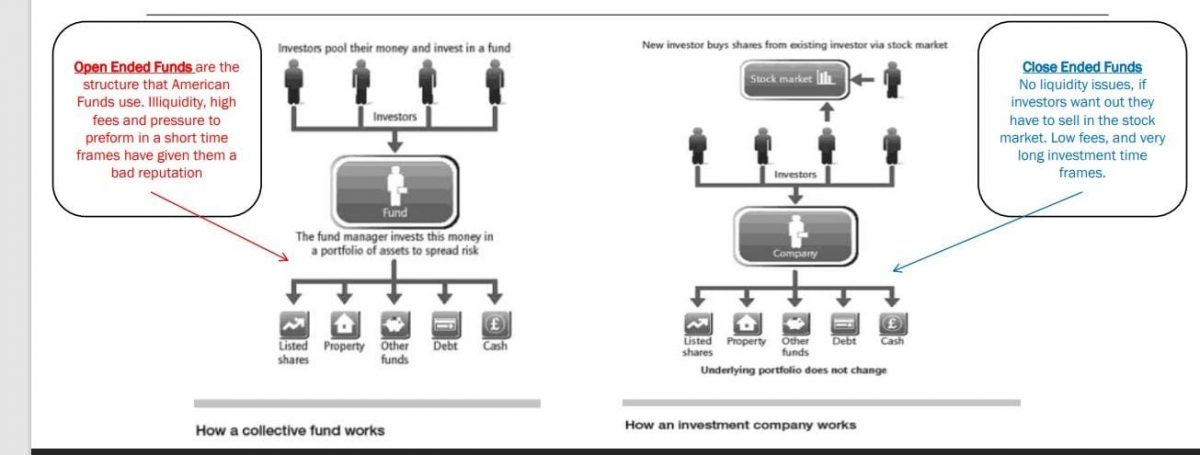

– They are (Public) Limited Companies also know as Close Ended Funds.

– There is NO deemed disposal Tax on Close Ended Funds.

B – What they are not

– They are not, Open-Ended Investment Company (OEICs) or Unit trusts. Note ETFs are also Open

Ended Funds.

– There is deemed disposal Tax on ALL Open Ended Funds.

Close ended Funds only have a limited number of shares in issue and hence “closed ended”.

They are traded on the London Stock Exchange in most cases.

All open ended funds are subject to Deemed Disposal Tax, irrespective of being managed or passive funds.

The Irish Revenue has never provided any clarification on the tax treatment of investment trusts and these fund types are not defined in the Revenue’s guidelines.

IRISH TAX POINTS WORTH NOTING

ETFs do not qualify for CGT credit of 1270/yea

ETFs are subject to 41% on gains and dividends

ETFs are subject to 8 year deemed disposal

Note: ETF’s require the investor to keeping track of deemed disposals which can prove complicated if there is not a system to keep track of purchase dates and costs in a spreadsheet.

Being required to pay tax every 8 years in Ireland clearly affects returns and the ability for it to compound!

Stocks are eligible for CGT credit of 1270/year

Stocks are taxed at 33% on gains and income tax rate for dividends (Same as ITs)

Stocks do not have deemed disposals

03 – How Investment Trusts work.

Eg Keystone Positive Change (0.55%) Positive social and environmental change.

Capital Reserves are on of the more important advantages that Trust have over open ended funds. More about them later.

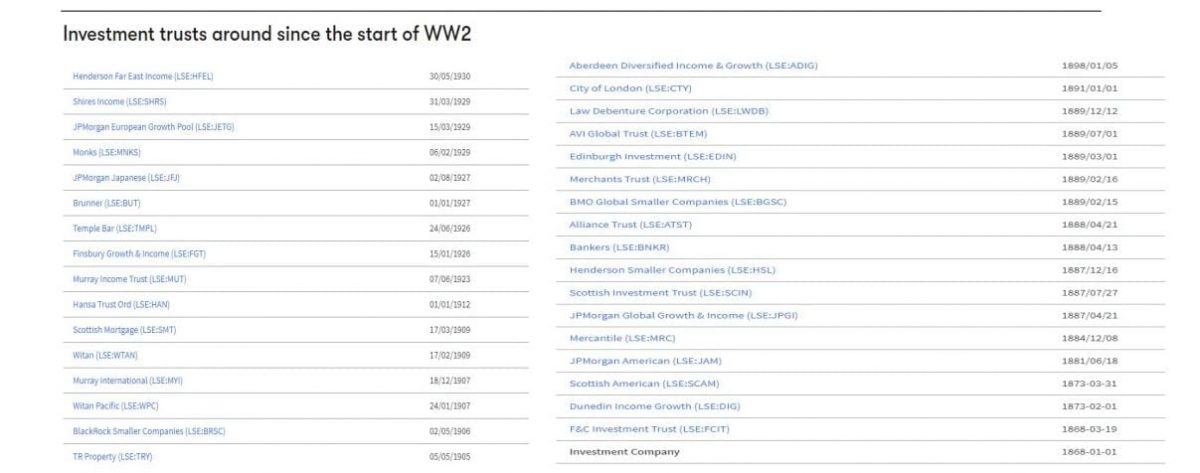

(30+ Investment Trust which are trading more than 85 Years)

01 – As a limited company all trusts have a board of directors and investment manager answer to the

board. (different from a OEIC)

02 – Investment Managers are often from separate companies who tender, via lower fees and

alternative investment approach for this role.

03 – Trusts can apply Gearing (i.e. get loans) to capitalise on opportunities.

04 – Trust are valued on Net Asset Value (NAV)

05 – As Trusts trade on the open market they often trade at a Discount or a Discount to NAV.

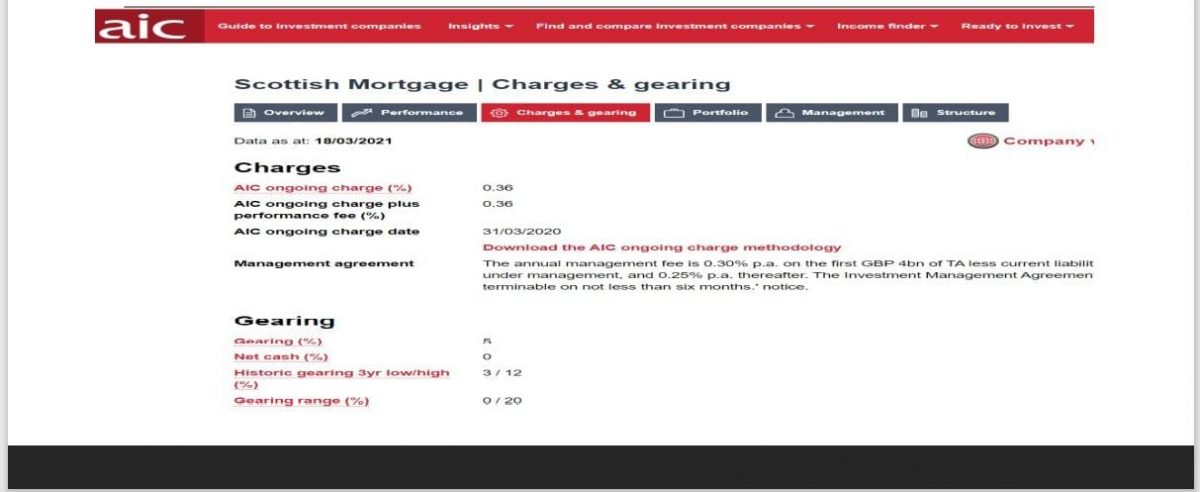

06 – Fees – Trusts charge fees as a %. The larger the trust, usually the lower the fee. E.g. SMT has an

ongoing fee of 0.36% per yr. Or City of London at 0.39%.

07 – Trusts can hold Capital Reserves, unlike open ended funds.

Information taken from AIC website:

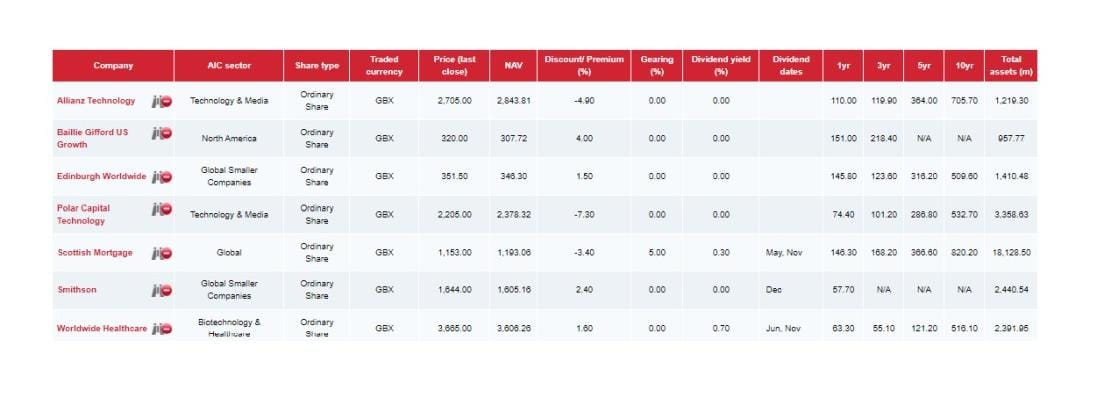

Note: 1% of 18 Billion is 180 Million Pounds!

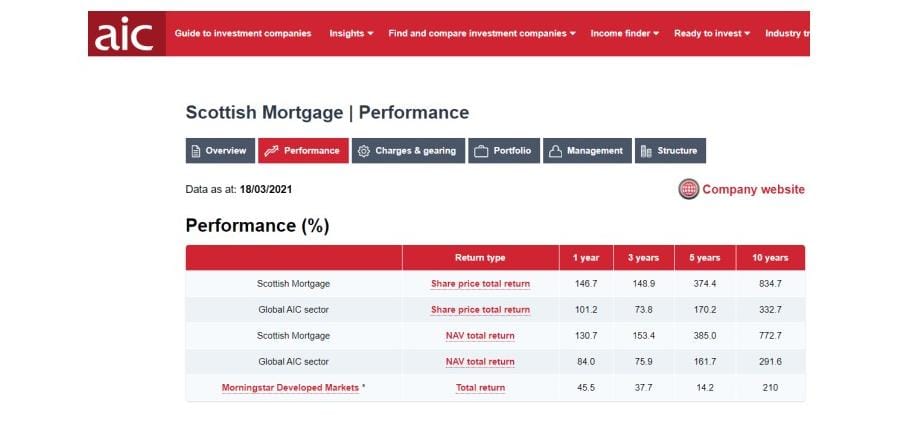

Scottish Mortgage – Performance

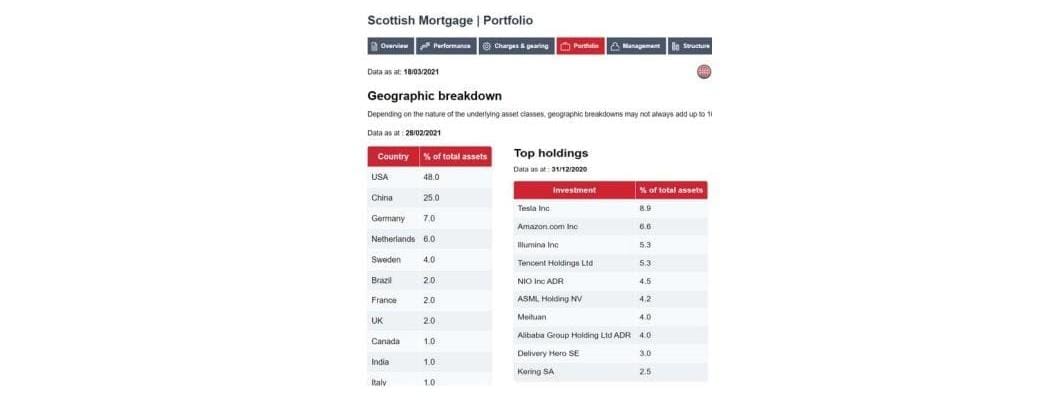

Scottish Mortgage – Portfolio: Geographic Breakdown & Top Holdings

Scottish Mortgage – Performance

Scottish Mortgage – Charges & Gearing

Asset Breakdown

04 – Pros and Cons of Investment Trusts.

The AIC ran a study from 2009 to 2019 and they found that out of 13 indexes studied IT bet there bench mark 9 out of 13 times.

05 – Some examples of Investment Trusts.

AIC Sectors:

– UK

– Overseas

– Flexible

– Specialist

– Property

– Debt

– VCT

Note: UK Income Tax and Corporation Tax – Once 90% distributed as dividend

Other Sectors not included:

Specialist (15 Sub sections)

– Leasing (Aeroplane Engines)

– Royalties (Hipgnosis Songs)

– Hedge Funds

Royalties

VCT – Venture Capital Trusts (Tax Advantaged)

– UK income tax and Corporation Tax

06 – Dividend Heroes & Non Dividend Paying Options

Dividend Heroes

Dividend Heroes are investment companies that have consistently increased their dividends for 20 or more years in a row.

Recent research from the AIC found that 85% of equity income-paying investment companies increased or maintained their dividends in 2020 compared to 23% of of income-paying open ended funds.

Dividend Heroes –

Saved by Capital Reserves, Trusts are allowed store up to 15% of there annual margin into there capital reserve to bolster there dividend payments for bad years.

Non Dividend Paying Options

Points Worth Noting:

Roughly 80% of the 400 IT pay out dividends.

These are good set and forgets.

No Dividend = no income tax liability

A good equivalent to an accumulating etf without the exit tax liability.

If investment theme become redundant they move onto something new. Scottish mortgage got started investing in rubber plantation for this new Car industry which needed tyres.

07 – Irish Investors & Taxation of Funds

01 – The Internet is full of misguided rubbish concerning this point.

02 – Research indicates the Irish Revenue has never provided any clarification on the tax

treatment of investment trusts and these fund types are not defined in the Revenue’s guidelines

03 – Investment trusts are companies and are governed by the Companies Act and not regulators

04 – Real Estate Investment Trusts (REITs) were introduced by section 41, of the Finance Act 2013.

(Revenue Guidance Document Part 25A-00-01). So (IT) type is defined for tax.

05 – So at present it can be assumed that dividend income on investment trusts is taxed at your

marginal rate of income tax, gains are taxed at the CGT tax rate of 33%, losses can be offset

against gains and losses can be carried forward.

As a view point it seems impossible to distinguish between IT and any quoted company, if it could be done perhaps they would have taxed them by now.

If they do it in the future it will be like the US ETFs in 2018.

08 – ETF v Investment Trusts (IT) Fees Model (Comparison table)

A common topic discussed is that ITs are significantly better than ETFs as an investment vehicle and this spreadsheet sets out to confirm if that is true.

Here we can compare how an ETF and IT perform under similar conditions (deposit, and growth). After a fixed number of years (20) we can compare which worked out better. We can also play around with different contribution / management fee structures to see what effect it will play on the overall result.

The IT table is straight forward as it just tracks growth less fees over time, with TAX becoming payable at the end.

ETFs are quite different due to the 8 year deemed disposal rules. This table is broken up into eight different groupings. Each grouping tracks deposits that take place every 8 years, also the tax for those deposits and the growth over time for that segment of the overall ETF. At the end of the 20 year period, the tax for all groupings becomes due (total withdrawal) so that we can compare the final result with the IT.

The result is a lot closer than would have been expected and it clearly highlights how the small management fee has a really large impact on the overall growth of the IT. (note: the excel document may not be 100% correct, so please use it for observational purposes only)

The following criteria are tracked (Year, Contribution Amount, Growth, Tax and Fund Amount, ETF/IT Contribution Fee, ETF/IT Management Fee, ETF/IT Tax)

To view this comparison table in full click here

*Credit to Alan Roche and David Mulligan both members of the local Limerick Financial Independence meet up groups for kindly sharing the comparison table excel document and allowing use for the Fire Dave blog, thank you*

To summarise the authors believe there is not much between the two and ETFs fare better in a lot of cases despite the higher tax unless you go for an IT with fees at the very low end or ones that out perform the market over the long term!

Case Study 2:

*Credit also to Jorge for adding additional case study on tabs 2 and 3 *

On the first tab, you can filter the ETFs and the ITs by fee and returns, and it tells you the average fee and return of the ETFs/ITs that match the filters, and how many they are.

Jorge found the best 4 ETFs by using (max fee: 0.15%, min return: 20%) and the best 4 ITs using (max fee: 0.6%, min return 20%). Makes no difference, ITs still on top.

Again to view the tabs click here

Check out Scottish Mortgage over a 5 year period 2017 – 2022 click here

It seems Investment Trusts are hard to ignore for the Irish investor!

Final – You can invest in Investment Trusts in DEGIRO.

1. Open your account here

2. Verify ID

3. Lodge funds